The 5D Model of RWA Tokenization

A new framework for designing real-world programmable asset systems that scale across jurisdictions and asset classes.

Tokenization is entering its “infrastructure decade.” From stablecoins to tokenized treasuries, invoice pools to community credit funds - the lines between traditional finance and programmable assets are blurring fast.

But there’s a fundamental problem: every RWA (Real World Asset) project still feels bespoke.

Each one rebuilds its own compliance stack, legal wrapper, and technical architecture from scratch. Teams spend months recreating the same primitives - KYC workflows, SPV formation, token standards - each slightly modified for a specific use case or jurisdiction.

It’s like trying to build global finance without accounting standards.

At Quantra, we’re developing a way to make this space modular and repeatable: a framework to describe any real-world asset system using a simple, structured blueprint.

We call it the 5D Model of RWA Tokenization.

Why Five Dimensions?

Real-world assets are inherently multidimensional. Each one isn’t just a token on a blockchain - it’s a contractual claim living within specific legal, financial, and technical contexts.

Change the context (move from India to the UAE, or from property to credit), and the entire design must adapt. What the industry needs is a universal schema that remains consistent across contexts while allowing customization at the edges.

That’s exactly what the 5D Model provides.

It defines every RWA system through five foundational dimensions:

The Five Dimensions

1. Asset Type - What’s being tokenized?

This defines the economic model underlying the token:

Yield-bearing credit

Stable reserve

Physical property

Community deposit pool

Carbon credits

The asset type determines how value is generated, priced, and distributed to token holders.

2. Jurisdiction - Where does the law apply?

An RWA isn’t global by default - it’s grounded in a legal system:

SEBI (India)

SEC (United States)

DFSA (Dubai)

MAS (Singapore)

MiCA (European Union)

Jurisdiction dictates:

What entity types can issue tokens

Who can hold them

Required reporting obligations

Transfer restrictions

3. Issuer Type - Who’s responsible for the asset?

Every RWA has an accountable entity:

Fund manager

NBFC (Non-Banking Financial Company)

SPV (Special Purpose Vehicle)

DAO

Community trust

Regulated bank

The issuer determines the governance and fiduciary model - how decisions are made, who can modify rules, and how audits are performed.

4. Distribution Model - Who can access the tokens?

This shapes the compliance perimeter:

Public: Open to retail investors

Accredited: Restricted to qualified investors

Private: Closed to verified community members

Institutional: Limited to corporate entities

Each model requires different KYC/AML procedures and compliance checks.

5. Instrument Structure - How is the asset represented on-chain?

The actual token model - how real-world rights map to digital tokens:

Technical components:

Token standard (ERC-20, ERC-3643, ERC-4626, ERC-1400)

Legal linkage (SPV shares, bond certificates, deposit claims)

Cashflow logic (interest payments, redemptions, default handling)

Real-World Examples

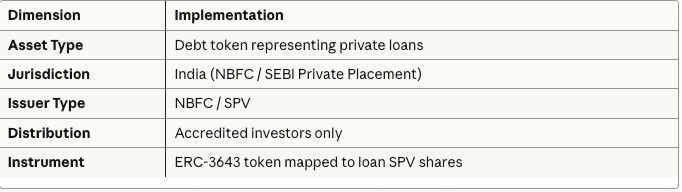

Example 1: Private Credit Fund (India)

Lifecycle:

Issuer onboards with KYC and SPV documentation

Loans deployed via SPV, each backed by an ERC-3643 token

Accredited investors subscribe via whitelist gateway

Repayments flow through payout scheduler, logged in audit trail

Compliance engine enforces transfer restrictions and investor caps

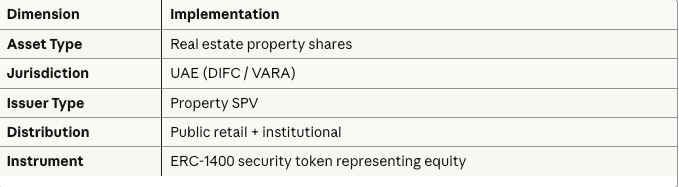

Example 2: Fractional Real Estate (UAE)

Lifecycle:

Developer SPV registers property and uploads legal documentation

Investors complete KYC verification, purchase fractional shares

Property revenue (rent, resale gains) distributed to token holders

Compliance inspector enforces UAE transfer restrictions

Regular filings via regulatory reporting engine

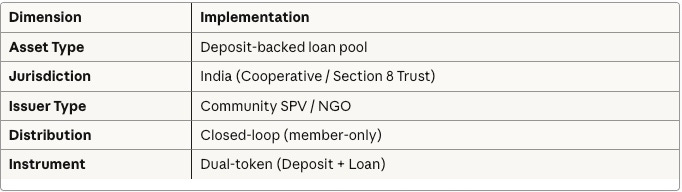

Example 3: Community Treasury (India → Africa)

Lifecycle:

Members deposit funds → mint Deposit Tokens (DT)

Treasury issues microloans to verified members → generates Loan Tokens (LT)

Interest and repayments distributed to DT holders

Governance: members vote on lending rules and reserve ratios

Audit log maintains compliance trail

Adaptability: This template extends to Kenya (SACCO), Nigeria (Cooperative Society), or Ghana (Credit Union) with minimal modifications.

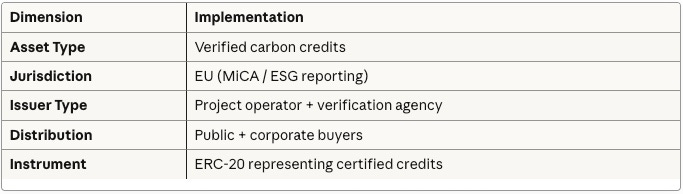

Example 4: Carbon Credit Pool (EU)

Lifecycle:

Carbon project uploads verification reports

Tokens minted and distributed through whitelist + ESG compliance

Automatic reporting aligned with EU disclosure requirements

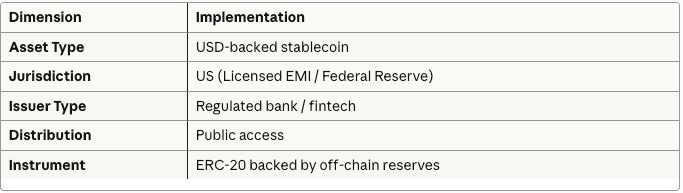

Example 5: USD Stablecoin (United States)

Lifecycle:

Users deposit USD → stablecoins minted

Redemptions trigger AML/KYC checks and reserve audits

Real-time yield managed via oracle

Full SEC/FinCEN compliance reporting

The Complete RWA Profile

When you combine the five dimensions, you get a complete RWA profile - a structured definition that determines which platform modules to activate.

Every RWA in Quantra is defined as a 5D Profile:

id: community-treasury-IN

asset_type: deposit_loan_pool

jurisdiction: IN

issuer_type: community_spv

distribution_model: member_only

instrument_structure: dual_token

modules:

- kyc-registry

- compliance-engine

- token-factory

- payout-scheduler

- audit-log

This profile automatically triggers the right modules for:

Onboarding

Compliance

Issuance

Servicing

Governance

Reporting

User Lifecycles

Issuer Journey: Onboards → defines asset → configures tokens → distributes → manages cashflows → reports

Investor Journey: Onboards → discovers offerings → invests → tracks portfolio → redeems/trades → generates tax reports

Regulator Journey: Accesses logs → simulates compliance scenarios → reviews filings

Developer Journey: Defines 5D profile → compiles compliance → deploys infrastructure → integrates with apps

Why This Matters

Tokenization isn’t simply about putting assets on-chain. It’s about translating legal, financial, and human trust into programmable structures.

The 5D Model provides a repeatable grammar - one that works equally well for:

A private credit fund in India

Fractional real estate in Dubai

Community microfinance in Africa

Carbon credit markets in the EU

USD-backed stablecoins in the US

Instead of rebuilding everything from scratch, teams can now configure their RWA system by selecting values across these five dimensions.

The Path Forward

As tokenization scales, we need shared standards - not just for tokens, but for the entire system architecture around them.

The 5D Model is our contribution to that infrastructure layer. It’s designed to make RWA development:

Faster (weeks instead of months)

Safer (built-in compliance by design)

More interoperable (common language across jurisdictions)

We’re building the blueprint standard that makes tokenization repeatable

Want to discuss how the 5D Model applies to your use case? Reach out to contact@quantra.finance